Abstract

Background: This study evaluated financial barriers limiting the growth and sustainability of agro-dealers in Zambia's Central Province. It also examined the impact of these challenges on the agricultural supply chain, assessed the adequacy of existing financial services, and investigated the role of government policies, financial institutions, and development programs in facilitating or hindering access to finance. Methods: Using a cross-sectional design, the study surveyed 384 agro-dealers. Data were collected through structured questionnaires and analyzed using descriptive statistics and logistic regression models to identify predictors of credit access and sales impact. Results: Major financial barriers identified were high interest rates (80.2%), collateral requirements (85.1%), and complex application processes (76.8%). These barriers led to inadequate stock (87.2%), lost sales (82.0%), and reduced product quality (50.8%). Logistic regression showed high interest rates significantly increased credit access (AOR = 6.68) and increased sales impact likelihood (AOR = 5.71). Collateral requirements also increased sales impact likelihood (AOR = 4.07). Thematic analysis highlighted inadequate government support, stringent lending criteria, and limited development program reach. Conclusions: The study highlights the need for targeted interventions, including simplifying application processes, developing tailored financial products, increasing government support, and enhancing development program reach. These measures are crucial for improving agro-dealers' financial stability and growth, thereby strengthening Zambia's agricultural sector and economy.

Keywords

Agro-dealers, Financial Barriers, Credit Access

1. Introduction

In Africa, agriculture is a vital economic sector, employing 65-70 percent of the continent's population and accounting for 20-40 percent of its GDP

| [18] | Making Finance Work for Africa. (2024). Enhancing Agricultural Finance in Africa. MFW4A Publications. |

[18]

. The sector is projected to become a $1 trillion industry by 2030, yet it receives less than 3% of banking credit

| [18] | Making Finance Work for Africa. (2024). Enhancing Agricultural Finance in Africa. MFW4A Publications. |

[18]

. Smallholder farms, which form the backbone of African agriculture, are particularly affected by limited access to finance, hindering their productivity and growth. The Mastercard Foundation notes that less than five percent of net bank lending goes to agriculture, with smallholder farmers being the most underserved

| [18] | Making Finance Work for Africa. (2024). Enhancing Agricultural Finance in Africa. MFW4A Publications. |

[18]

. This financial exclusion has significant implications for the sector's ability to meet the continent's food demands and contribute to economic development.

Zambia's agricultural sector is a critical component of the national economy, contributing about 19 percent to GDP and employing three-quarters of the population

| [13] | International Trade Organisation. (2022). The Impact of Financial Barriers on Agricultural Supply Chains. ITO Reports. |

[13]

. The sector is diverse, encompassing crops, livestock, and fisheries, with small-scale farmers representing approximately 90 percent of Zambia’s agricultural producers

| [14] | Kabwe, G., Machina, H., & Kinkese, K. (2018). Financial Inclusion and Challenges for Agro-Dealers in Zambia. Zambian Agricultural Journal. |

| [13] | International Trade Organisation. (2022). The Impact of Financial Barriers on Agricultural Supply Chains. ITO Reports. |

| [20] | Ngoma, B. (2023). Financial Access Issues in Rural Zambia. Journal of Rural Studies. |

[14, 13, 20]

. Despite having vast arable land and water resources, only a fraction is under cultivation, and the sector remains predominantly rain-fed

| [13] | International Trade Organisation. (2022). The Impact of Financial Barriers on Agricultural Supply Chains. ITO Reports. |

[13]

. The Zambian government has recognized the need to diversify the economy and has identified agriculture as a key driver for this change

| [29] | Stiglitz, J. E., & Weiss, A. (1981). Credit rationing in markets with imperfect information. The American Economic Review, 71(3), 393-410. Retrieved from Credit Rationing in Markets with Imperfect Information on JSTOR. |

[29]

.

Access to finance remains a significant barrier for Zambian farmers, particularly for start-ups and small-scale agro-dealers

. The World Bank's Agriculture Finance Diagnostic for Zambia highlights that less than 3 percent of small- and medium-scale farmers have access to formal sector credit

. This lack of financial inclusion limits farmers' ability to invest in inputs, technology, and infrastructure, thereby constraining their productivity and market competitiveness.

2. Literature Review

2.1. Global Perspective

Challenges in Agricultural Finance

Global barriers include high interest rates, collateral demands, and limited credit access, which stifle the growth of agricultural businesses.

2.2. Role of International Financial Institutions

International Financial Institutions (IFIs) such as the World Bank and the Food and Agriculture Organization (FAO) significantly influence agricultural finance globally. These organizations support economic and social development in developing countries and promote international economic cooperation

. The World Bank, for example, assists in designing and developing a range of financial instruments that empower poor farmers and facilitate the development of food value chains

. The FAO focuses on increasing the resilience of agricultural systems against potential crises and improving the efficiency of agricultural production

| [10] | Food and Agriculture Organization. (2023). Credit to agriculture: Global and regional trends 2013–2022. FAOSTAT Analytical Brief No. 76. https://doi.org/10.4060/cc9027en |

[10]

.

Despite a 13% increase in global credit to agriculture between 2013 and 2022, the share of agriculture in total credit has slightly decreased, indicating a growing recognition of the sector's needs but also highlighting the challenges in keeping pace with other sectors

| [10] | Food and Agriculture Organization. (2023). Credit to agriculture: Global and regional trends 2013–2022. FAOSTAT Analytical Brief No. 76. https://doi.org/10.4060/cc9027en |

[10]

.

2.3. Global Trends in Agricultural Finance

Globally, the demand for agricultural financing exceeds $400 billion annually just for working capital

. However, the sector often remains underfunded, particularly in regions where agriculture forms the backbone of the economy. The Asian region, for example, has seen a substantial increase in the amount of credit provided to agriculture, led mainly by countries like China and India

| [10] | Food and Agriculture Organization. (2023). Credit to agriculture: Global and regional trends 2013–2022. FAOSTAT Analytical Brief No. 76. https://doi.org/10.4060/cc9027en |

[10]

.

2.4. Challenges and Innovations in Agricultural Finance

2.4.1. Common Challenges

One of the primary challenges in agricultural finance is risk assessment. Agriculture is inherently risky due to factors such as weather variability, pests, diseases, and market fluctuations

| [29] | Stiglitz, J. E., & Weiss, A. (1981). Credit rationing in markets with imperfect information. The American Economic Review, 71(3), 393-410. Retrieved from Credit Rationing in Markets with Imperfect Information on JSTOR. |

[29]

. These risks make financial institutions wary of lending to farmers, particularly smallholders who might lack the collateral or credit history to secure loans

.

Political risks also pose significant challenges. Government intervention and interference can be unpredictable and can affect the stability and predictability of agricultural finance

. Additionally, the lack of infrastructure and data in rural areas further complicates the delivery of financial services

.

2.4.2. Innovations Addressing Challenges

Fintech innovations have emerged as critical solutions to these challenges, offering new ways to extend financial services to underserved farmers. Digital platforms and mobile technology enable farmers to access financial services such as loans, insurance, and payment systems directly from their devices, which is particularly beneficial in remote areas

. These platforms use alternative data for credit scoring, which can include mobile phone usage patterns, transaction histories, and even satellite imagery

.

Blockchain technology and smart contracts are also being explored for their potential to provide transparency and reduce transaction costs in agricultural finance

. These technologies can help streamline supply chains, ensure prompt payments to farmers, and provide verifiable data on agricultural practices, which can be used to assess risk more accurately.

In summary, while the global agricultural finance landscape faces significant challenges, particularly in terms of risk management and access to finance, innovations in fintech are providing new pathways to address these issues. International financial institutions like the World Bank and FAO play crucial roles in supporting these developments and in promoting sustainable agricultural practices worldwide.

2.4.3. Innovations in Finance

Emerging fintech solutions, such as mobile banking and digital credit platforms, are improving access to finance for farmers in underserved regions

.

2.5. Regional Perspective (Africa)

Agriculture is pivotal to Africa's economy, significantly contributing to the Gross Domestic Product (GDP) and employing a majority of the continent's population. In Sub-Saharan Africa, agriculture transcends mere economic activity; it is a way of life, providing sustenance, employment, and income for billions. The sector is projected to grow into a $1 trillion industry by 2030, underscoring its potential to drive economic growth and alleviate poverty

| [18] | Making Finance Work for Africa. (2024). Enhancing Agricultural Finance in Africa. MFW4A Publications. |

[18]

. Despite its importance, the agricultural sector in Africa faces numerous challenges that impede its productivity and growth.

Key challenges include high interest rates charged by financial institutions, which significantly restrict farmers' access to necessary financial resources for investing in inputs and technology. Additionally, the lack of collateral is a considerable barrier, as most farmers do not possess sufficient assets to secure loans, exacerbating their financial exclusion

| [6] | Coomes, D. (2023). Impact of Rural and Agricultural Finance in Sub-Saharan Africa. School Policy Analysis & Research Group (EPAR). Retrieved from https://epar.evans.uw.edu/blog/impact-rural-and-agricultural-finance-sub-saharan-africa |

| [15] | Khan, F. U., Nouman, M., Negruț, L., Abban, J., Cismaș, L. M., & Siddiqi, M. F. (2024). Constraints to agricultural finance in underdeveloped and developing countries: a systematic literature review. International Journal of Agricultural Sustainability, 22(1). https://doi.org/10.1080/14735903.2024.2329388 |

| [27] | Sacerdoti, E. (2005). Access to Bank Credit in Sub-Saharan Africa: Key Issues and Reform Strategies. IMF Working Paper No. 05/166. Retrieved from https://www.imf.org/external/pubs/ft/wp/2005/wp05166.pdf |

[6, 15, 27]

. These financial constraints not only limit the growth and sustainability of agricultural enterprises but also affect the broader agricultural economy and supply chain in the region.

Central and Southern Africa

The agricultural sector in Southern and Central Africa plays a pivotal role in the economic and social fabric of the region. However, it remains underutilized in many countries within the region, facing significant economic challenges, including poverty reduction, food security, employment creation, and the sustainable use of natural resources

. Adverse weather conditions and recurrent droughts further exacerbate food insecurity, impacting farm-level food production and threatening the livelihoods of millions across the region

.

Additionally, climate change poses further threats, with projections indicating reduced rainfall, increased temperatures, and high variability, potentially leading to reductions in agricultural productivity by 15% to 50%

| [21] | Nhemachena, C., Nhamo, L., Matchaya, G., Nhemachena, C., Muchara, B., Karuaihe, S., & Mpandeli, S. (2020). Climate change impacts on water and agriculture sectors in Southern Africa: Threats and opportunities for sustainable development. Water, 12(10), 2673. https://doi.org/10.3390/W12102673 |

[21]

.

Zambia, a country within Southern Africa, is endowed with a large arable land resource base of 42 million hectares, of which only 1.5 million hectares are cultivated annually

.

Zambia has a relatively large number of microfinance institutions (MFIs) that play a crucial role in providing financial services to underserved populations, including smallholder farmers and agro-dealers. MFIs offer small loans, savings facilities, and capacity-building services to their clients. Over the years, the growth of MFIs in Zambia has been attributed to addressing the credit gaps, particularly for marketeers and small-scale entrepreneurs in the agricultural sector

| [5] | Chibbonta, D., & Chishimba, H. (2023). Effects of microfinance services on the livelihoods of marketeers in Zambia: A case of Matero market in Lusaka. Cogent Social Sciences, 9(2). https://doi.org/10.1080/23311886.2023.2266922 |

[5]

.

2.6. Financial Barriers in Agriculture

In Sub-Saharan Africa, farmers and agro-dealers face challenges like credit inaccessibility, poor infrastructure, and a lack of financial literacy, which limit their growth potential

| [15] | Khan, F. U., Nouman, M., Negruț, L., Abban, J., Cismaș, L. M., & Siddiqi, M. F. (2024). Constraints to agricultural finance in underdeveloped and developing countries: a systematic literature review. International Journal of Agricultural Sustainability, 22(1). https://doi.org/10.1080/14735903.2024.2329388 |

[15]

.

2.7. Continental Initiatives

Programs from institutions like the African Development Bank (AfDB) are driving efforts to provide financial solutions for smallholder farmers, but progress is slow due to policy gaps and implementation challenges

.

3. Methodology

3.1. Research Design

This study utilized a mixed-method research design combining quantitative and qualitative approaches. Surveyed 384 agro-dealers using structured questionnaires and logistic regression analysis to identify predictors of credit access.

3.2. Scope of the Study

The study was geographically limited to Zambia's Central Province, focusing on start-up entrepreneurs and agro-dealers within the agricultural sector. It encompasses an analysis of financial barriers, the impact of these challenges on the agricultural supply chain, and the adequacy of existing financial services. The study also examined the role of government policies, financial institutions, and development programs in influencing access to finance for agro-dealers.

3.3. Study Population

The study focused on agro-dealers within Zambia's Central Province, actively operating and registered with local agricultural or business associations for legitimacy.

3.4. Data Collection

Primary data was obtained by administration of structured questionnaires addressing demographic characteristics, business types, and financial challenges.

Secondary Data: Reviewed agricultural reports to supplement primary data.

3.5. Sample Size

The sample size of 384 agro-dealers was determined based on the Cochran formula

| [30] | Taherdoost, H. (2016). Sampling Methods in Research Methodology; How to Choose a Sampling Technique for Research. International Journal of Academic Research in Management (IJARM), 5(2), 18-27. |

[30]

, which considers the expected frequency of the outcome, the desired level of precision, and the population size. Using a 95% confidence level and a 5% margin of error, the sample size is calculated as follows:

Where:

n is Sample size

Z is the z-score corresponding to the level of confidence (1.96 for 95% confidence).

P is the estimated prevalence of first aid knowledge (50%, assuming no prior data).

E is the margin of error (0.05 for 5%)

4. Data Analysis

Descriptive Statistics: Summarized data on demographic characteristics and financial barriers.

Inferential Statistics: Logistic regression analysis to explore predictors of credit access and sales impact.

Thematic Analysis: Analyzed qualitative data on experiences and perceptions of financial barriers.

Ethical Considerations:

Ethical approval obtained from the University of Zambia’s Biomedical Research Ethics Committee (UNZABREC). Informed consent ensured confidentiality and voluntary participation.

1. Existing financial services and products available to Agro-dealers in the Central Province.

Descriptive Statistics

Table 1. Types of Financial Services Used.

Financial Service | Frequency | Percent |

Use of Financial Services – None | 149 | 38.8% |

Use of Financial Services - Bank Loans | 75 | 19.5% |

Use of Financial Services - Microfinance Loans | 125 | 32.6% |

Use of Financial Services - Government Grants | 20 | 5.2% |

Use of Financial Services - Credit from Suppliers | 271 | 70.6% |

Use of Financial Services - Overdraft Facilities | 247 | 64.3% |

Source: Field Survey, 2024

Credit from suppliers (70.6%) and overdraft facilities (64.3%) are the most commonly used financial services, with limited reliance on bank loans (19.5%).

Specific financial barriers that limit the growth and sustainability of agro-dealers in the Central Province.

Descriptive Statistics:

Table 2. Financial Barriers Faced.

Financial Barrier | Frequency | Percent |

High Interest Rates | 308 | 80.2% |

Collateral Requirements | 325 | 85.1% |

Complex Application Processes | 295 | 76.8% |

Lengthy Approval Times | 287 | 74.7% |

Lack of Information on Services | 177 | 46.5% |

Credit History Requirements | 228 | 59.4% |

Distance to Facilities | 168 | 43.8% |

No Barriers Faced | 50 | 13.2% |

Source: Field Survey, 2024

Collateral requirements (85.1%), high interest rates (80.2%), Complex Application Processes (76.8%) and Lengthy Approval Times (74.7%) are the most significant financial barriers faced by agro-dealers in the Central Province.

2. Specific financial barriers that limit the growth and sustainability of agro-dealers in the Central Province.

Inferential Statistics:

Table 3. Multivariable Logistic Regression Analysis for Predicting Factors Associated with Credit Access.

Predictor | Adjusted Odds Ratio (95% CI) | p-value |

High Interest Rates | 6.68 (2.98, 14.95) | 0.000 |

Lengthy Approval Times | 0.12 (0.04, 0.34) | 0.000 |

Credit History Requirements | 2.58 (1.43, 4.65) | 0.002 |

Source: Field Survey, 2024

High interest rates significantly increase credit access (AOR = 6.68, p = 0.000), while lengthy approval times decrease it (AOR = 0.12, p = 0.000). A good credit history also improves access (AOR = 2.58, p = 0.002).

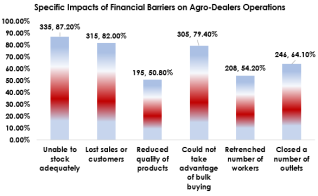

3. Impact of financial challenges on the agricultural supply chain and the broader agricultural economy in the region.

Descriptive Statistics:

Figure 1. Specific Impacts of Financial Barriers on Agro-Dealers Operations.

The most significant impacts are the inability to stock adequately (87.2%) and lost sales or customers (82.0%).

Inferential Statistics:

Table 4. Multivariable Logistic Regression Analysis for Predicting Factors Associated with Sales Impact.

Predictor | Adjusted Odds Ratio (95% CI) | p-value |

High Interest Rates | 5.71 (1.80, 18.06) | 0.003 |

Collateral Requirements | 4.07 (1.47, 11.21) | 0.007 |

Accessibility to Financial Services | 0.40 (0.28, 0.57) | 0.000 |

Source: Field Survey, 2024

High interest rates significantly increase the likelihood of negative sales impacts by 5.71 times (p = 0.003). Similarly, collateral requirements increase this risk by 4.07 times (p = 0.007). Conversely, better accessibility to financial services reduces the likelihood of sales impacts by 60% (AOR = 0.40, p = 0.000).

4. Investigate the role of government policies, financial institutions, and development programs in facilitating or hindering access to finance for Agro-dealers:

Thematic Analysis:

Role of Government Policies, Financial Institutions, and Development Programs in Access to Finance

Government Policies and Financial Institutions

Government Policies:

1. Limited Implementation: Poor implementation and bureaucratic delays hinder the effectiveness of government financial programs aimed at agro-dealers.

2. Lack of Awareness: Few agro-dealers participate in government/NGO programs due to limited outreach.

3. Regulatory Barriers: Strict compliance requirements further restrict access to government-backed financial programs.

Financial Institutions:

1. Stringent Lending Criteria: High collateral demands and credit history requirements make it difficult for agro-dealers to access loans.

2. Lack of Tailored Products: Traditional financial products are not suited to the seasonal nature of agricultural businesses.

3. High Interest Rates: Most of the agro-dealers cite high interest rates as a major obstacle to accessing finance.

Development Programs:

1. Capacity Building: Programs provide financial literacy training, helping agro-dealers improve their creditworthiness.

2. Access to Grants: Limited reach of development programs as only 30.7% of agro-dealers participate, despite the potential benefits like grants and subsidies.

3. Networking Opportunities: Development programs foster collaboration and partnerships that can improve financial access.

5. Discussion of Findings

Financial Barriers Limiting Agro-Dealers' Growth

1. High Interest Rates and Collateral Requirements

1) Key Findings:

80.2% of respondents identified high interest rates as a major financial barrier; 85.1% of respondents struggled with collateral requirements.

2) Statistical Insight:

Agro-dealers facing high interest rates were significantly more likely to access credit (AOR = 6.68, p < 0.001), while collateral requirements significantly hindered access.

3) Triangulation:

These findings align with global studies, which show that high interest rates and stringent collateral demands limit the growth of SMEs, particularly in agriculture

| [4] | Berger, A. N., & Udell, G. F. (2006). A more complete conceptual framework for SME finance. Journal of Banking & Finance, 30(11), 2945-2966. https://doi.org/10.1016/j.jbankfin.2006.05.008 |

| [11] | Gorodnichenko, Y., & Schnitzer, M. (2013). Financial constraints and innovation: Why poor countries don't catch up. Journal of the European Economic Association, 11(5), 1115-1152. https://doi.org/10.1111/jeea.12033 |

[4, 11]

.

2. Application Processes and Approval Times

1) Key Findings:

76.8% of respondents reported complex loan application processes, while 74.7% highlighted lengthy approval times as barriers.

2) Statistical Insight:

Lengthy approval times significantly reduced the likelihood of accessing credit (AOR = 0.12, p < 0.001).

3) Triangulation:

These results echo findings that cumbersome procedures and approval delays reduce access to finance for SMEs

| [16] | Kira, A. R. (2013). Determinants of financing constraints in East African countries' SMEs. International Journal of Business and Management, 8(8), 49-68. https://doi.org/10.5539/ijbm.v8n8p49 |

| [22] | Olomola, A. S. (2014). Business Operations of Agrodealers and Their Participation in the Loan Market in Nigeria. IFPRI Discussion Paper 01400. International Food Policy and Research Institute. |

| [23] | Olomola, A. S. (2014). Determinants of agro-dealers’ participation in the loan market in Nigeria. International Food and Agribusiness Management Review, 17(3), 65-84. |

[16, 22, 23].

Impact of Financial Services and Role of Policies

3. Financial Services Available to Agro-Dealers

1) Key Findings:

Only 19.5% of respondents used bank loans, while 70.6% relied on supplier credit, which offered more flexibility.

2) Statistical Insight:

Microfinance loans were used by 32.6% of respondents, though barriers like limited availability and high costs persist.

3) Triangulation:

This aligns with research showing that traditional banking services are underutilized in agriculture, while supplier credit remains crucial for liquidity

| [2] | Beck, T. (2007). Financing constraints of SMEs in developing countries: Evidence, determinants, and solutions. Journal of International Money and Finance, 31(2), 401-441. |

[2]

.

4. Role of Government Policies and Development Programs

1) Key Findings:

5.2% of agro-dealers accessed government grants; most cited bureaucratic inefficiencies and lack of awareness as barriers.

2) Statistical Insight:

Respondents with better access to development programs and financial services were significantly less likely to face sales impacts (AOR = 0.40, p < 0.001).

3) Triangulation:

These findings are consistent with studies that emphasize the role of government support and development programs in facilitating access to finance for SMEs

| [12] | International Fertilizer Development Center (IFDC). (2012). Nigeria Agro-Dealer Support (NADS) Project Summary. Abuja, Nigeria. |

| [29] | Stiglitz, J. E., & Weiss, A. (1981). Credit rationing in markets with imperfect information. The American Economic Review, 71(3), 393-410. Retrieved from Credit Rationing in Markets with Imperfect Information on JSTOR. |

[12, 29]

.

6. Conclusion

1. High Prevalence of Financial Barriers:

80.2% of agro-dealers face high interest rates; 85.1% encounter collateral requirements, and 76.8% report complex loan application processes as significant barriers.

2. Significant Operational Impacts:

Financial constraints disrupt the agricultural supply chain, resulting in inadequate stock (87.2%), lost sales (82.0%), and reduced product quality (50.8%).

3. Limited Utilization of Financial Services:

Only 19.5% of agro-dealers use bank loans, while 32.6% access microfinance loans. Government grants are rarely utilized, with only 5.2% of respondents benefitting.

4. Role of Government and Financial Institutions:

Low participation in government and NGO programs (5.2% accessed grants) and poor accessibility to financial services (27.9% rate access as very poor).

5. Thematic Analysis Highlights:

Simplifying loan application processes, offering tailored financial products, and increasing government and institutional support are critical to addressing financial challenges for agro-dealers.

Abbreviations

AfDB | African Development Bank |

FAO | Food and Agriculture Organisation |

GDP | Gross Domestic Product |

IFIs | International Financial Institutions |

NGO | Non-Government Organisation |

MFIs | Micro Financial Institutions |

SMEs | Small and Medium Enterprise |

UNZABREC | University of Zambia’s Biomedical Research Ethics Committee |

Acknowledgments

A special recognition to Mr. Chishimba Boniface, Mr. Mutakila Sutcliffe, and Mr. Kapeya Robert for the technical support rendered to this study during data collection by purposively guiding us to other agro-dealers for administration of the questionnaires.

Author Contributions

Nicholus Obby Mainza: Writing-original draft, Editorial, Conceptualization, Resources, Validation, Project administration, Visualization, and Funding.

Chipego Kafunga Hachinene: Methodology, Data curation, Formal Analysis, and Software.

Funding

This work is not supported by any external funding, all the necessary financial matters and resources were covered by the corresponding author.

Data Availability Statement

The data is available from the corresponding author upon reasonable request.

Conflicts of Interest

There is no conflict of interest for this paper. The only possible conflict of interest for future study could be the sources for primary data collection of which this research targeted agro-dealers and start-up entrepreneurs only.

References

| [1] |

Bhargava, V. (2006). The Role of the International Financial Institutions in Addressing Global Issues. Retrieved from

https://gbdrrrf.org/system/files/privatefiles/international_financial_institutions_ifis.pdf

|

| [2] |

Beck, T. (2007). Financing constraints of SMEs in developing countries: Evidence, determinants, and solutions. Journal of International Money and Finance, 31(2), 401-441.

|

| [3] |

Benni, N. (2023). Fintech innovation for smallholder agriculture. Food and Agriculture Organization of the United Nations. Retrieved from

https://www.fao.org/3/cc9117en/cc9117en.pdf

|

| [4] |

Berger, A. N., & Udell, G. F. (2006). A more complete conceptual framework for SME finance. Journal of Banking & Finance, 30(11), 2945-2966.

https://doi.org/10.1016/j.jbankfin.2006.05.008

|

| [5] |

Chibbonta, D., & Chishimba, H. (2023). Effects of microfinance services on the livelihoods of marketeers in Zambia: A case of Matero market in Lusaka. Cogent Social Sciences, 9(2).

https://doi.org/10.1080/23311886.2023.2266922

|

| [6] |

Coomes, D. (2023). Impact of Rural and Agricultural Finance in Sub-Saharan Africa. School Policy Analysis & Research Group (EPAR). Retrieved from

https://epar.evans.uw.edu/blog/impact-rural-and-agricultural-finance-sub-saharan-africa

|

| [7] |

Enterprise Zambia Challenge Fund. (2021). Financial Barriers in Zambia’s Agricultural Sector. Enterprise Zambia Reports.

|

| [8] |

European Commission. (2023). Financial Constraints in Agriculture: A European Perspective. European Commission Reports.

|

| [9] |

Ferreira, P. (2023). Fintech in Agriculture: How Digital Platforms are Empowering Farmers. Retrieved from

https://www.financemagnates.com/fintech/fintech-in-agriculture-how-digital-platforms-are-empowering-farmers/

|

| [10] |

Food and Agriculture Organization. (2023). Credit to agriculture: Global and regional trends 2013–2022. FAOSTAT Analytical Brief No. 76.

https://doi.org/10.4060/cc9027en

|

| [11] |

Gorodnichenko, Y., & Schnitzer, M. (2013). Financial constraints and innovation: Why poor countries don't catch up. Journal of the European Economic Association, 11(5), 1115-1152.

https://doi.org/10.1111/jeea.12033

|

| [12] |

International Fertilizer Development Center (IFDC). (2012). Nigeria Agro-Dealer Support (NADS) Project Summary. Abuja, Nigeria.

|

| [13] |

International Trade Organisation. (2022). The Impact of Financial Barriers on Agricultural Supply Chains. ITO Reports.

|

| [14] |

Kabwe, G., Machina, H., & Kinkese, K. (2018). Financial Inclusion and Challenges for Agro-Dealers in Zambia. Zambian Agricultural Journal.

|

| [15] |

Khan, F. U., Nouman, M., Negruț, L., Abban, J., Cismaș, L. M., & Siddiqi, M. F. (2024). Constraints to agricultural finance in underdeveloped and developing countries: a systematic literature review. International Journal of Agricultural Sustainability, 22(1).

https://doi.org/10.1080/14735903.2024.2329388

|

| [16] |

Kira, A. R. (2013). Determinants of financing constraints in East African countries' SMEs. International Journal of Business and Management, 8(8), 49-68.

https://doi.org/10.5539/ijbm.v8n8p49

|

| [17] |

Köhn, D., & Jainzik, M. (2014). Food security and a holistic finance for rural markets. In Springer eBooks.

https://doi.org/10.1007/978-3-642-54034-9_2

|

| [18] |

Making Finance Work for Africa. (2024). Enhancing Agricultural Finance in Africa. MFW4A Publications.

|

| [19] |

NEPAD. (2013). African agriculture, transformation and outlook. Retrieved from

https://www.tralac.org/images/docs/6460/agriculture-in-africa-transformation-and-outlook.pdf

|

| [20] |

Ngoma, B. (2023). Financial Access Issues in Rural Zambia. Journal of Rural Studies.

|

| [21] |

Nhemachena, C., Nhamo, L., Matchaya, G., Nhemachena, C., Muchara, B., Karuaihe, S., & Mpandeli, S. (2020). Climate change impacts on water and agriculture sectors in Southern Africa: Threats and opportunities for sustainable development. Water, 12(10), 2673.

https://doi.org/10.3390/W12102673

|

| [22] |

Olomola, A. S. (2014). Business Operations of Agrodealers and Their Participation in the Loan Market in Nigeria. IFPRI Discussion Paper 01400. International Food Policy and Research Institute.

|

| [23] |

Olomola, A. S. (2014). Determinants of agro-dealers’ participation in the loan market in Nigeria. International Food and Agribusiness Management Review, 17(3), 65-84.

|

| [24] |

Rooyen, J. (1997). Challenges and roles for agriculture in the Southern African region. Agrekon, 36(3), 181-205.

https://doi.org/10.1080/03031853.1997.9523459

|

| [25] |

Rooyen, J., & Sigwele, H. (1998). Towards regional food security in southern Africa: A (new) policy framework for the agricultural sector. Food Policy, 23(6), 491-504.

https://doi.org/10.1016/S0306-9192(98)00057-8

|

| [26] |

Ruete, M. (2015). Financing for Agriculture: How to boost opportunities in developing countries. International Institute for Sustainable Development. Retrieved from

https://www.iisd.org/system/files/publications/financing-agriculture-boost-opportunities-developing-countries.pdf

|

| [27] |

Sacerdoti, E. (2005). Access to Bank Credit in Sub-Saharan Africa: Key Issues and Reform Strategies. IMF Working Paper No. 05/166. Retrieved from

https://www.imf.org/external/pubs/ft/wp/2005/wp05166.pdf

|

| [28] |

Saluoks, R. (2022). Agrifinance Trends For 2023: Breaking Down Barriers. Retrieved from

https://www.globalaginvesting.com/agrifinance-trends-2023-breaking-barriers/

|

| [29] |

Stiglitz, J. E., & Weiss, A. (1981). Credit rationing in markets with imperfect information. The American Economic Review, 71(3), 393-410. Retrieved from Credit Rationing in Markets with Imperfect Information on JSTOR.

|

| [30] |

Taherdoost, H. (2016). Sampling Methods in Research Methodology; How to Choose a Sampling Technique for Research. International Journal of Academic Research in Management (IJARM), 5(2), 18-27.

|

| [31] |

Varangis, P., Buchenau, J., & Ono, T. (2018). Agricultural Finance: Agricultural Finance and Agricultural Insurance As part of National Financial Inclusion Agendas. Retrieved from

https://thedocs.worldbank.org/en/doc/901541553199006646-0130022019/render/NFISSession20RuralandAgriculturalConsumers.pdf

|

| [32] |

The World Bank. (2018). Zambia: Harvesting Agricultural Potential. Retrieved from

https://www.worldbank.org/en/about/partners/brief/zambia-harvesting-agricultural-potential

|

| [33] |

The World Bank Group. (2019). Zambia - Agriculture Finance Diagnostic. Retrieved from

https://documents1.worldbank.org/curated/en/241301582041593315/pdf/Agriculture-Finance-Diagnostic-Zambia.pdf

|

| [34] |

The World Bank. (2022). Agriculture Finance & Agriculture Insurance. Retrieved from

https://www.worldbank.org/en/topic/financialsector/brief/agriculture-finance

|

| [35] |

Zambia Development Agency. (2024). Agriculture. Retrieved from

https://www.zda.org.zm/agriculture/

|

Cite This Article

-

APA Style

Mainza, N. O., Hachinene, C. K. (2024). Challenges Faced by Start-up Entrepreneurs in Agriculture Sector to Access Finance: A Case of Agro-dealers in Zambia's Central Province. Humanities and Social Sciences, 12(6), 202 -209. https://doi.org/10.11648/j.hss.20241206.13

Copy

|

Copy

|

Download

Download

ACS Style

Mainza, N. O.; Hachinene, C. K. Challenges Faced by Start-up Entrepreneurs in Agriculture Sector to Access Finance: A Case of Agro-dealers in Zambia's Central Province. Humanit. Soc. Sci. 2024, 12(6), 202 -209. doi: 10.11648/j.hss.20241206.13

Copy

|

Download

AMA Style

Mainza NO, Hachinene CK. Challenges Faced by Start-up Entrepreneurs in Agriculture Sector to Access Finance: A Case of Agro-dealers in Zambia's Central Province. Humanit Soc Sci. 2024;12(6):202 -209. doi: 10.11648/j.hss.20241206.13

Copy

|

Download

-

@article{10.11648/j.hss.20241206.13,

author = {Nicholus Obby Mainza and Chipego Kafunga Hachinene},

title = {Challenges Faced by Start-up Entrepreneurs in Agriculture Sector to Access Finance: A Case of Agro-dealers in Zambia's Central Province

},

journal = {Humanities and Social Sciences},

volume = {12},

number = {6},

pages = {202 -209},

doi = {10.11648/j.hss.20241206.13},

url = {https://doi.org/10.11648/j.hss.20241206.13},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.hss.20241206.13},

abstract = {Background: This study evaluated financial barriers limiting the growth and sustainability of agro-dealers in Zambia's Central Province. It also examined the impact of these challenges on the agricultural supply chain, assessed the adequacy of existing financial services, and investigated the role of government policies, financial institutions, and development programs in facilitating or hindering access to finance. Methods: Using a cross-sectional design, the study surveyed 384 agro-dealers. Data were collected through structured questionnaires and analyzed using descriptive statistics and logistic regression models to identify predictors of credit access and sales impact. Results: Major financial barriers identified were high interest rates (80.2%), collateral requirements (85.1%), and complex application processes (76.8%). These barriers led to inadequate stock (87.2%), lost sales (82.0%), and reduced product quality (50.8%). Logistic regression showed high interest rates significantly increased credit access (AOR = 6.68) and increased sales impact likelihood (AOR = 5.71). Collateral requirements also increased sales impact likelihood (AOR = 4.07). Thematic analysis highlighted inadequate government support, stringent lending criteria, and limited development program reach. Conclusions: The study highlights the need for targeted interventions, including simplifying application processes, developing tailored financial products, increasing government support, and enhancing development program reach. These measures are crucial for improving agro-dealers' financial stability and growth, thereby strengthening Zambia's agricultural sector and economy.

},

year = {2024}

}

Copy

|

Download

-

TY - JOUR

T1 - Challenges Faced by Start-up Entrepreneurs in Agriculture Sector to Access Finance: A Case of Agro-dealers in Zambia's Central Province

AU - Nicholus Obby Mainza

AU - Chipego Kafunga Hachinene

Y1 - 2024/11/21

PY - 2024

N1 - https://doi.org/10.11648/j.hss.20241206.13

DO - 10.11648/j.hss.20241206.13

T2 - Humanities and Social Sciences

JF - Humanities and Social Sciences

JO - Humanities and Social Sciences

SP - 202

EP - 209

PB - Science Publishing Group

SN - 2330-8184

UR - https://doi.org/10.11648/j.hss.20241206.13

AB - Background: This study evaluated financial barriers limiting the growth and sustainability of agro-dealers in Zambia's Central Province. It also examined the impact of these challenges on the agricultural supply chain, assessed the adequacy of existing financial services, and investigated the role of government policies, financial institutions, and development programs in facilitating or hindering access to finance. Methods: Using a cross-sectional design, the study surveyed 384 agro-dealers. Data were collected through structured questionnaires and analyzed using descriptive statistics and logistic regression models to identify predictors of credit access and sales impact. Results: Major financial barriers identified were high interest rates (80.2%), collateral requirements (85.1%), and complex application processes (76.8%). These barriers led to inadequate stock (87.2%), lost sales (82.0%), and reduced product quality (50.8%). Logistic regression showed high interest rates significantly increased credit access (AOR = 6.68) and increased sales impact likelihood (AOR = 5.71). Collateral requirements also increased sales impact likelihood (AOR = 4.07). Thematic analysis highlighted inadequate government support, stringent lending criteria, and limited development program reach. Conclusions: The study highlights the need for targeted interventions, including simplifying application processes, developing tailored financial products, increasing government support, and enhancing development program reach. These measures are crucial for improving agro-dealers' financial stability and growth, thereby strengthening Zambia's agricultural sector and economy.

VL - 12

IS - 6

ER -

Copy

|

Download